Tracey Allway writes: Is there a relationship between the subprime mortgage crash and the disorderly fall in the price of oil.

Created in January 2006 and consisting of a basket of credit default swaps (CDS) tied to the welfare of subprime mortgages, it allowed a bevy of investors to bet on the future direction of riskier home loans and helped inflate the massive amounts of leverage tied to the U.S. housing bubble. More recently it played a starring role in the film version of Michael Lewis’s The Big Short—when protagonists Christian Bale, Steve Carell, et al. are tracking their bets against the U.S. housing market, they are tracking the ABX.

Fast-forward to today and Bank of America analysts provide an update to their previous thesis, which was that the downward spiral in the price of oil was shaping up to look a lot like the negative trend that engulfed the subprime space circa the year 2007.

Here’s what they say:

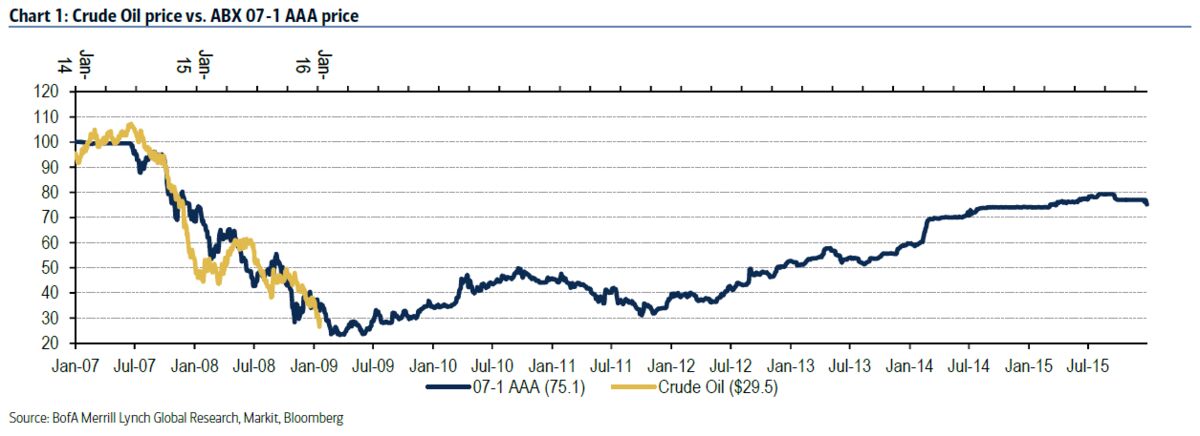

The pattern of the decline in the price of oil that began in mid-2014 is remarkably similar to the 2007-2009 pattern of the price decline of ABX, the credit derivative index that referenced subprime mortgages and, ultimately, the U.S. housing market (Chart 1). The ABX history suggests that oil will see more declines in the next couple of months and find a floor somewhere in the low 20s in the March-April time frame. Both the duration of the decline (1.5+ years) and the scale of the decline (100 neighborhood starting price down to the sub-30 neighborhood) are similar. Given that both housing and oil prices were fueled to spectacular heights in the two periods by massive credit expansion, it’s probably more than just coincidence that the respective “bubble” bursting patterns are so similar.

Consider how things tend to work. Denial on what constitutes fair value is a big component of bubbles, on the part of both market participants and policymakers. When perceived “bubbles” burst, markets take their time in steadily shredding views of the perception of fundamental value, as prices move lower and lower. Along the way, many will cite “technical factors” as the cause of the decline, which in some way suggests the price decline may not be real when in fact it is all too real. In the end, the technicals drive the fundamentals, as credit flees and borrowers go bust, and a feedback loop lower kicks in. Lower prices beget accelerated selling, as asset owners need to raise cash. It could be margin calls or it could be producer selling needs, it doesn’t really matter: the selling becomes inevitable and turns into forced selling.

The point here is not that oil is necessarily the new subprime crisis per se but that the recent action in the price of crude resembles nothing if not the bursting of a bubble and the sudden realization that the asset has been overvalued for too long. More worrying for oil investors will be BofAML’s idea of forced selling. As Flanagan notes: “The systemic margin call of 2008 seems to be back for now, albeit to a far lesser degree.”

.