Pass through businesses increase in US.

he importance of pass-through business entities has soared in the past three decades. Over the same period, the amount of pass-through business income flowing to the top 1 percent of income earners has increased sharply. Despite this profound change in the organization of U.S. business activity, we lack clean, clear facts about the consequences of this change for the distribution and taxation of business income.

Pass-through entities — partnerships, tax code subchapter S corporations, and sole proprietorships — are not subject to corporate income tax. Their income passes directly to their owners and is taxed under whatever tax rules those owners face. In contrast, the income of traditional corporations, more specifically subchapter C corporations, is subject to corporate income taxes, and after-tax income distributed from the corporation to its owners is also taxable.

In 1980, pass-through entities accounted for 20.7 percent of U.S. business income; by 2011, they represented 54.2 percent. Many partnerships are opaque. A fifth of partnership income was earned by partners that the study’s authors were not able to classify into one of several categories, such as a domestic individual or a foreign corporation. In addition, some partnerships are circular, in the sense that they are owned by other partnerships, which could in turn be owned by yet other partnerships.

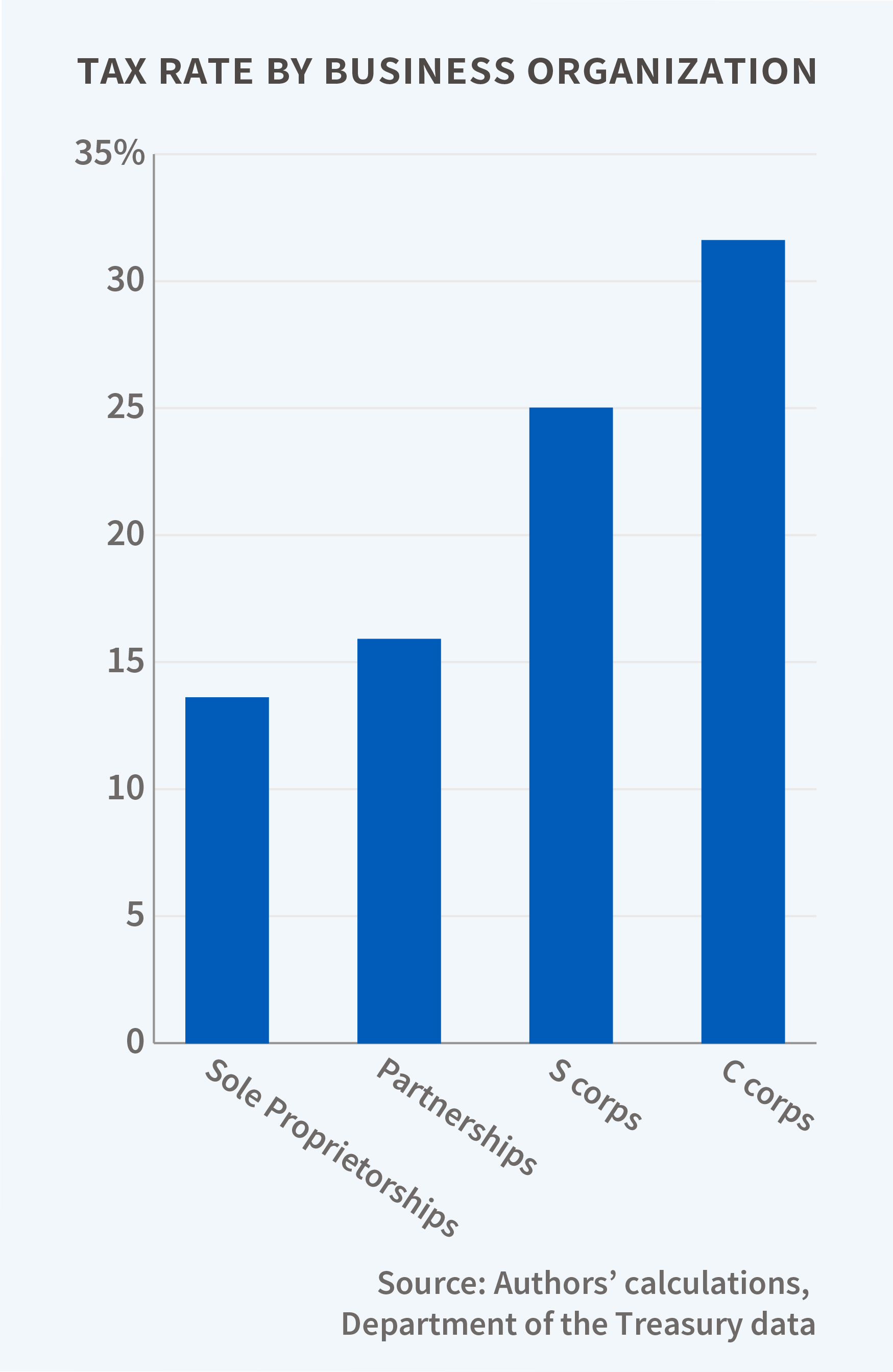

Pass-through business income faces lower tax rates than traditional corporate income. The tax rate on the income earned by pass-through partnerships is a relatively low 15.9 percent, excluding interest payments and unrepatriated foreign income. That compares with a 31.6 percent rate for C corporations and a 24.9 percent rate for S corporations. Only sole proprietorships have a lower average rate, 13.6 percent. Combining both taxes on corporations and taxes on investors, the researchers calculate that the U.S. business sector as a whole pays an average tax rate of 24.3 percent.

The lower average tax rate for pass-through entities than for traditional corporations translates into reduced federal revenues, the researchers conclude. They estimate that in 2011, if the share of pass-through tax returns had been at its 1980 level, when traditional C corporations and sole proprietorships dominated, the average rate would have been 3.8 percentage points higher and the Treasury would have collected $100 billion more in tax revenue.

One reason partnerships pay such a low average tax rate is that nearly half their income (45 percent) is classified as capital gains and dividend income, which is taxed at preferential rates. Another 15 percent of their income is earned by tax-exempt and foreign entities, for which the effective tax rate is less than five percent. The roughly 30 percent of partnership income that is earned by unidentifiable and circular partnerships is taxed at an estimated 14.7 percent rate.